JAG

Top 20

Question if a shareholder does not register his or her shares with Atomic where do they stand , and I might post a Sunday funny , I was travelling on Friday , no excuse uppercut for me

Question if a shareholder does not register his or her shares with Atomic where do they stand , and I might post a Sunday funny , I was travelling on Friday , no excuse uppercut for me

Ok this was a question for a mate I told him long ago to register so if his shares go POOF who the fuck gets them

Sorry mate, I wasn’t taking the piss.Ok this was a question for a mate I told him long ago to register so if his shares go POOF who the fuck gets them

I have said many times, TSE is the place for intel , respectful posting and swift extraction of trolls

That has been consistent throught this long arduous 3 yr journey.

AVZ TSE is in a league of its own.

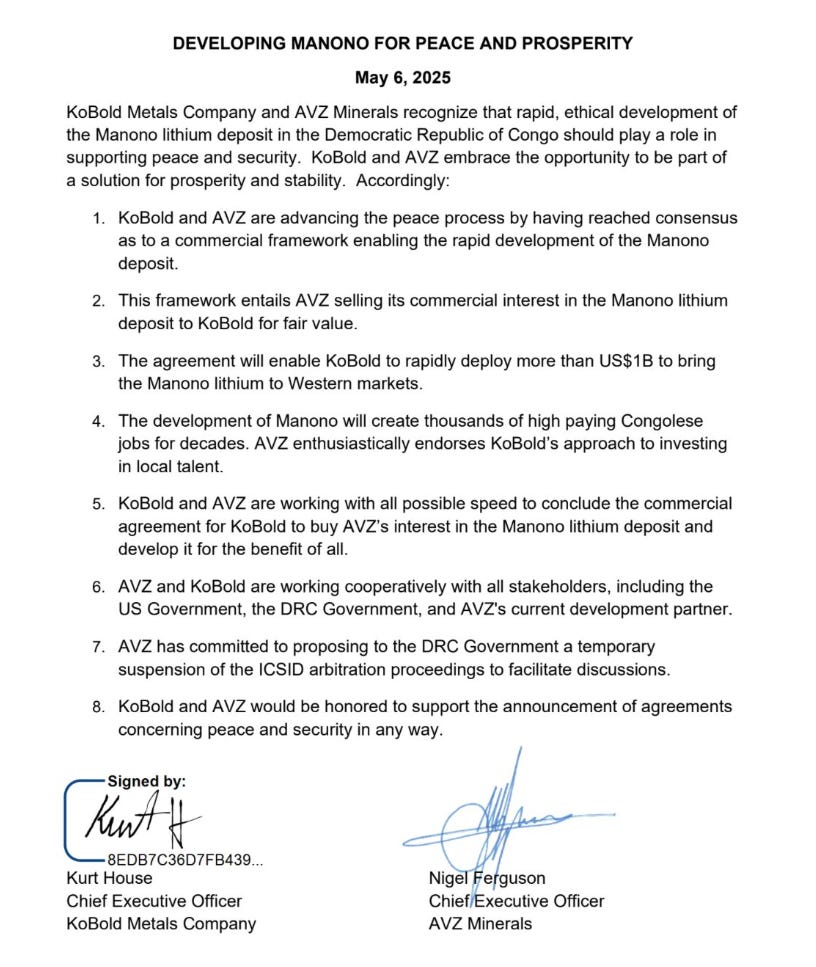

From the day Trump championed our cause it was clear the mineral/security deal was contingent on no Comminere or Chinese involvement in Manono(RD).Just imagine how much CATH-CATL could produce annually, and they offered us an option to acquire 49% interest in a Lithium Carbonate (LCE) conversion plant built by CATH

Can any of you imagine what sort of return that would give us shareholders, so as far as I’m concerned KoBold can stump up a fair price or fuck off

Almost 3000 pages since we all moved here for the better.

Let’s hope we all get along until the end & after I don’t know

We all end up in a better position after all this bullshit and still talk shit with each other.

Or go our separate ways and find the next full fuxked up drama share to get into

GLTAH

Do you really think we'll get a $2 partyAll comes down to what we get paid out I guess, would be nice if we finally got that $2 party. Send AVZ off with a bang and leave Nigel with the tab?

Avz = sc6

arcadium = LCE

Get it right dawg

Based on research, no company is having the capacity to have 200k LCE per year. Not even albermale

Comparing Arcadium is not a true comparison as brine is included. Its better to keep simple and compare hardrock and hardrock processing only. Opex is usually lower with Brine after capex, however the deposit that AVZ owns is brilliant, and Capex will be on lower side if conventional DMS is used and Opex is low due to jurisdiction.Arcadium Lithium’s mines in total produce 75,000 Tonnes of LCE annually.

I don’t know what AVZ’s yearly production would be but Roche Dure alone has 26Mt of LCE so if AVZ produced the same amount of LCE per year as Arcadium, it would give us a mine life of over 300 years. Of course that’s before KoBold’s so called amazing AI technology discovers there’s actually even more lithium than what AVZ has already measured, indicated and inferred

Just imagine how much CATH-CATL could produce annually, and they offered us an option to acquire 49% interest in a Lithium Carbonate (LCE) conversion plant built by CATH

Can any of you imagine what sort of return that would give us shareholders, so as far as I’m concerned KoBold can stump up a fair price or fuck off

My worst fears of late were that kobold had even approached avz, and got some kind of agreement, before the speculated usa discussions with drc...From the day Trump championed our cause it was clear the mineral/security deal was contingent on no Comminere or Chinese involvement in Manono(RD).

FT wont grant CATH a ML and risk jeopardising the minerals/security deal. Hence Kobold's cockiness and wrapping their ann with talk of peace and security. The subtext being: only the US via Kobold can provide Felix the deal he craves.

Therefore the only counter-bids Nigel can realistically entertain are from non-Chinese companies, preferably US ones.

Not surprising, it was fairly amateurish.X post and Youtube video regarding Kobold Metals recent BBC World Service discussion about Manono have now been removed

Comparing Arcadium is not a true comparison as brine is included. It’s better to keep simple and compare hardrock and hardrock processing only. Opex is usually lower with Brine after capex, however the deposit that AVZ owns is brilliant, and Capex will be on lower side if conventional DMS is used and Opex is low due to jurisdiction.

Production should be considered in in terms of how much can be extracted and then processed. Considering the quality of the deposit and easy way to think of it is to divide by 6 or 7.

As an example

extracted and processed via DMS = 1.2mt extracted and processed per year.

SC6 produced from 1mt (1,200,000 / 6) = 240,000 Sc6

Approximately 7x Sc6 for 1tonne of Carbonate (240,000 / 7 ) = ~35,000 LCE per year

Its been sometime since I have looked at the studies for AVZ so I am not sure if they were targeting 4.5mt p/y, or a sulphate, either way its worth far more than what Arcadium sold for which, if you followed the background noise, was way too low a valuation backed by a management group who folded and didn't put up a fight.... Well done AVZ

Silly Seppo, doesn't he know the internet is forever?Not surprising, it was fairly amateurish.

substack.com

substack.com

Haha well there you have it not only is Cominiere out but US want a whole parallel public administration for US businesses (think of TV cop shows where the "feds" turn up and waive off the local cops" - no bribes or corruption for US businesses).

Last I heard AVZ was planning down to go to primary lithium sulfate on site. My use of SC6 was just for some napkin math. Given Besos wants lithium for his trucks, from Kobold to Slate will probably have some integrated chemical conversion/battery partnerships too (with amazon then shipping all the ancillary merch for the truck customizations).Avz is targeting 4mt SC6, not 4mt ore

Comparing Arcadium is not a true comparison as brine is included. Its better to keep simple and compare hardrock and hardrock processing only. Opex is usually lower with Brine after capex, however the deposit that AVZ owns is brilliant, and Capex will be on lower side if conventional DMS is used and Opex is low due to jurisdiction.

Production should be considered in in terms of how much can be extracted and then processed. Considering the quality of the deposit and easy way to think of it is to divide by 6 or 7.

As an example

extracted and processed via DMS = 1.2mt extracted and processed per year.

SC6 produced from 1mt (1,200,000 / 6) = 240,000 Sc6

Approximately 7x Sc6 for 1tonne of Carbonate (240,000 / 7 ) = ~35,000 LCE per year

Its been sometime since I have looked at the studies for AVZ so I am not sure if they were targeting 4.5mt p/y, or a sulphate, either way its worth far more than what Arcadium sold for which, if you followed the background noise, was way too low a valuation backed by a management group who folded and didn't put up a fight.... Well done AVZ

That’s back when AVZ was targeting mining 4.5Mt of ore annually, then they looked at expanding to 10Mt annually so you can take that 100,000 tonnes of LCE annually and more than double it to over 200,000 tonnes of LCE annually

That’s back when AVZ was targeting mining 4.5Mt of ore annually, then they looked at expanding to 10Mt annually so you can take that 100,000 tonnes of LCE annually and more than double it to over 200,000 tonnes of LCE annuallyYeah, I seem to recall that being the case for target ore production.AVZ’s targeted annual production was 700,000 tonnes of SC6 (lithium / spodumene concentrate) which equates to over 100,000 tonnes of LCE (lithium carbonate equivalent) annually. That’s at least 33% more than what Arcadium is producing from its mines